Jay Zhao and Jenny Xiao

May 22, 2024

[Full webinar deck available here.]

Many people have been asking us about our views on AI and enterprise SaaS: What defines an AI-first software company? How will AI reshape enterprise SaaS? How can startups compete with existing players? What are the challenges of building an AI-first enterprise SaaS product? How do AI application companies build enduring moats? These are critical questions for the future of AI because enterprise SaaS represents one of the biggest categories in software spending.

This webinar aims to address these common questions about AI and enterprise SaaS, proposing a thesis for investing in the next generation of enterprise SaaS products.

What is AI-First Enterprise SaaS

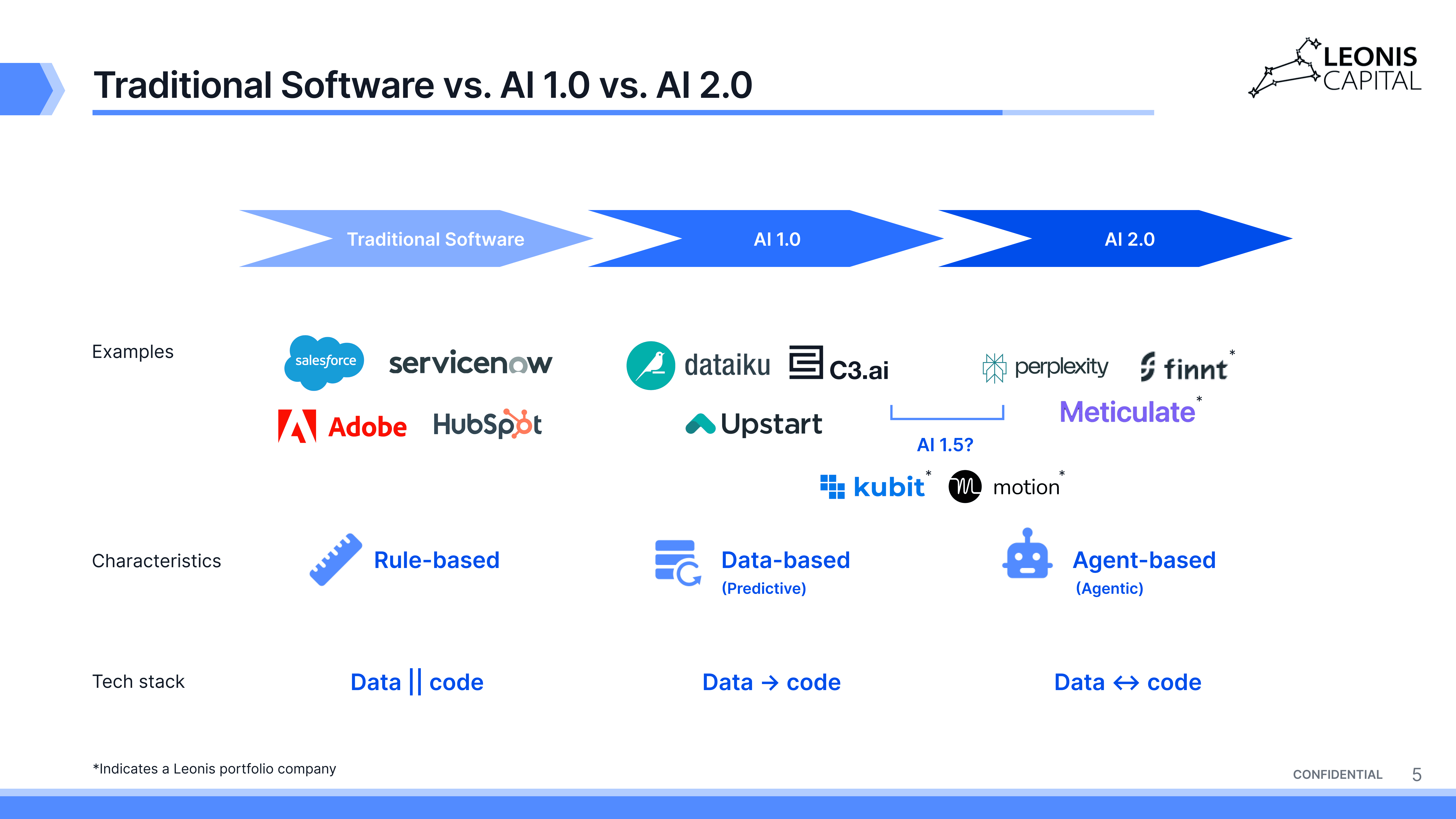

Enterprise SaaS has evolved through three generations: traditional software, AI 1.0, and AI 2.0. Traditional enterprise products, such as Salesforce and Adobe, rely on rule-based software where data and code are kept separate.

In traditional SaaS, software companies were built as “static databases” (e.g., Salesforce, Hubspot) where the data and code are largely separate. The software was mostly programmed to be rule-based, and end users primarily used SaaS for record-keeping (Salesforce) or single-pointed functions (Adobe). In the AI 1.0 era, data became an integral part of the code, forming the backbone of products. AI 1.0 software, powered by machine learning, had predictive characteristics—higher quality and quantity of data usually resulted in higher output accuracy (e.g., computer vision AI companies). The quality and quantity of their data often constituted the biggest moat for AI 1.0 companies.

When we first started Leonis, we noticed companies evolving beyond typical AI 1.0 solutions (like recommendation engines and classification algorithms). By 2021, the companies we invested in were becoming more autonomous, leveraging early-generation LLMs like GPT-3 to create products that made decisions on behalf of users. These companies demonstrated much stronger value propositions and ROI for end users. Motion and Kubit AI are examples of such AI 1.5 companies.

However, true AI 2.0 companies emerged with the release of more powerful models like GPT-4 and Claude-3. AI 2.0 enterprise SaaS products are characterized by their agency—their ability to be increasingly intelligent and autonomous. Startups can now leverage robust foundational APIs provided by companies like OpenAI and Anthropic to build workflow-specific or industry-specific agentic software. In AI 2.0 companies, LLM-powered synthetic data and co-pilot software that can also generate code result in data and code commingling, influencing and improving each other. Additionally, for the first time, software can have a “reflection” mechanism built in, allowing for compounded learning and improvement.

Both AI 1.0 and AI 2.0 companies fall into the AI-first category because they share similarities in their tech stack and team structures, distinct from traditional enterprise SaaS companies. We’ve elaborated on this in a previous research post in 2023. Consequently, AI 1.0 companies have transitioned into the AI 2.0 era more easily than traditional software companies, which struggle with fundamental tech stack incompatibilities and difficulties in hiring AI talent.

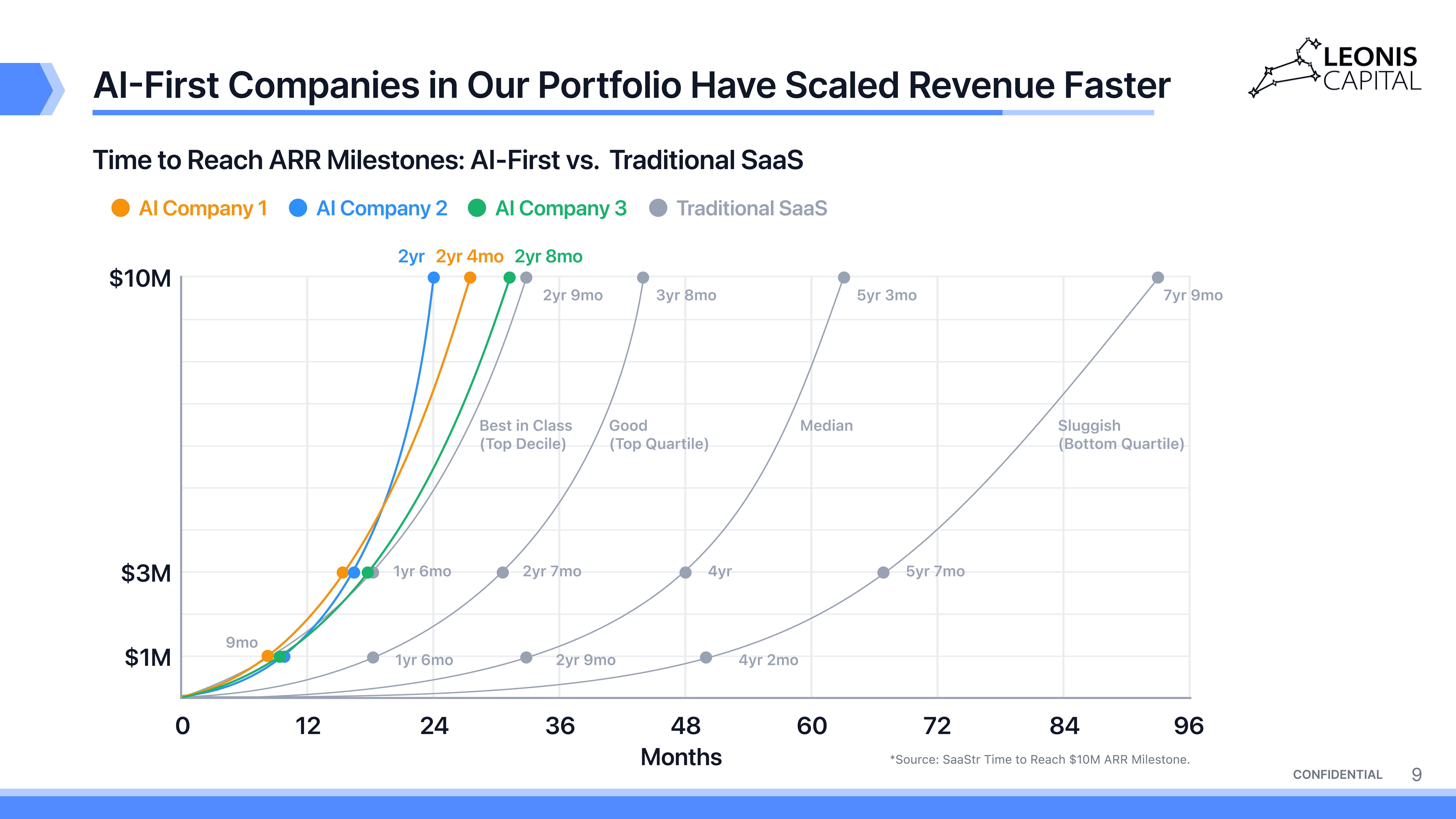

One observation from our portfolio companies is that AI-first companies can scale revenue much faster than traditional SaaS because AI offers a higher return on investment (ROI) for buyers and is more likely to produce significantly better results (e.g., ChatGPT versus previous chatbots).

The AI 2.0 era presents an even more attractive opportunity to build capital-efficient startups. With commoditized models, application-layer companies avoid the costs and challenges of training their own models. Off-the-shelf APIs reduce tech risks and eliminate the need to hire entire ML engineering teams.

Investing in AI-First Enterprise SaaS

Why invest in application-layer companies if models are controlled by providers? Can they capture value without owning their models? To answer this, we examined the revenue split percentage between application- and infrastructure-layer companies in the cloud era.

In 2003, application-layer companies generated 29% of total cloud software revenue. By 2023, their share increased to 39%, while the overall market grew exponentially. This indicates that application-layer companies have grown faster and captured significantly more value over time.

Today, application-layer companies in AI account for only 23% of total AI revenue, similar to the early dawn of the cloud era transition. However, over the next 20 years, we expect these companies to scale even faster and capture a larger share as the market expands.

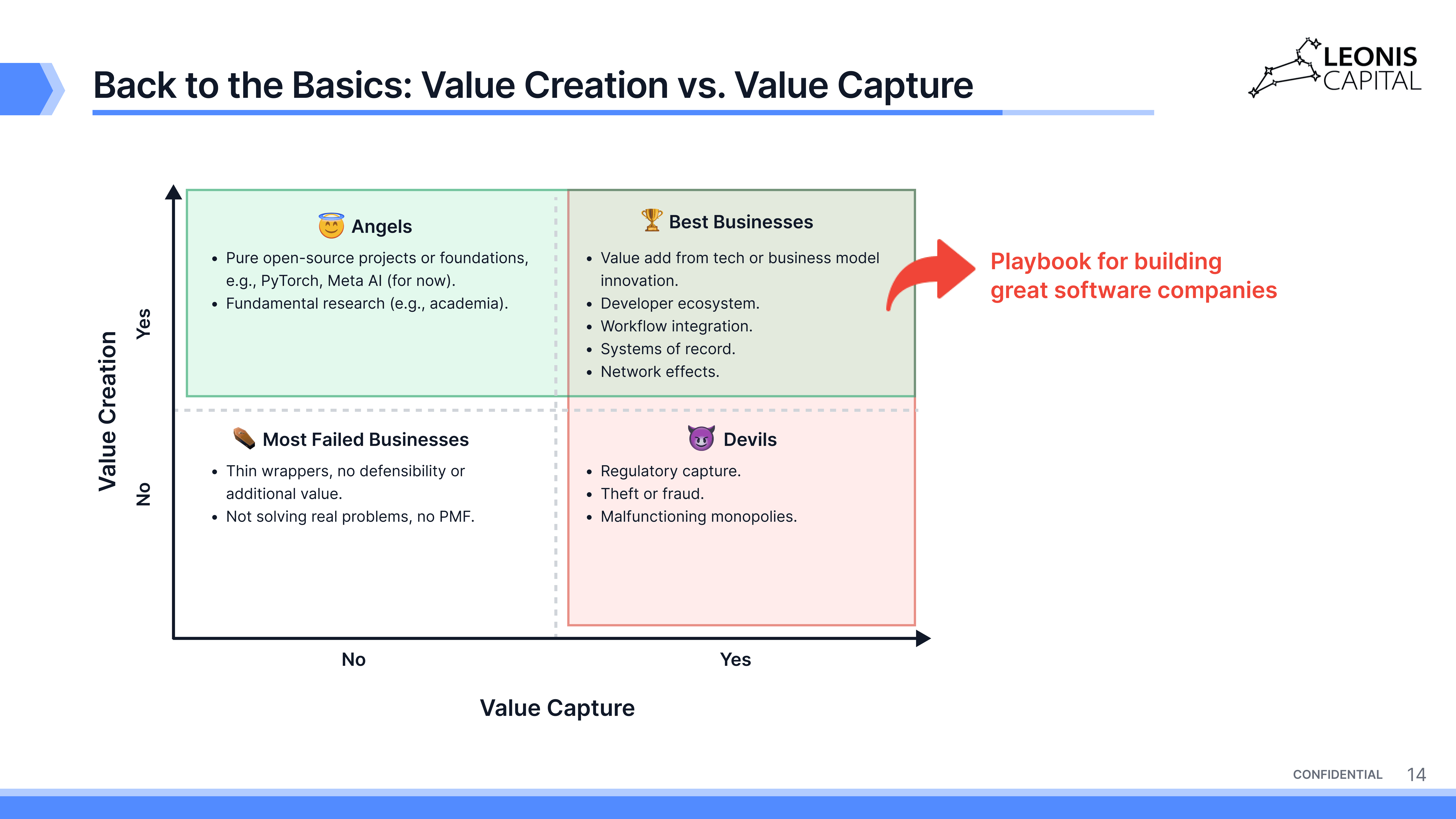

Before delving into our investment thesis, we introduce a simple framework for value creation and capture, categorizing companies into "angels," "devils," "failed businesses," and "best businesses." The slide gives you a more detailed description of these four kinds of businesses.

When we began exploring AI 2.0 companies in late 2022, they mainly fell into the “angels” or “failed businesses” categories, being either pure open-source projects or thin wrappers with little additional value. Founders believed AI was an entirely new category and didn't want to follow traditional SaaS playbooks.

In 2024, we're seeing more startups adopt tactics that helped traditional SaaS companies create and capture value, such as building developer ecosystems or integrating with enterprise workflows. Founders now understand that these strategies will help them build a moat and capture value.

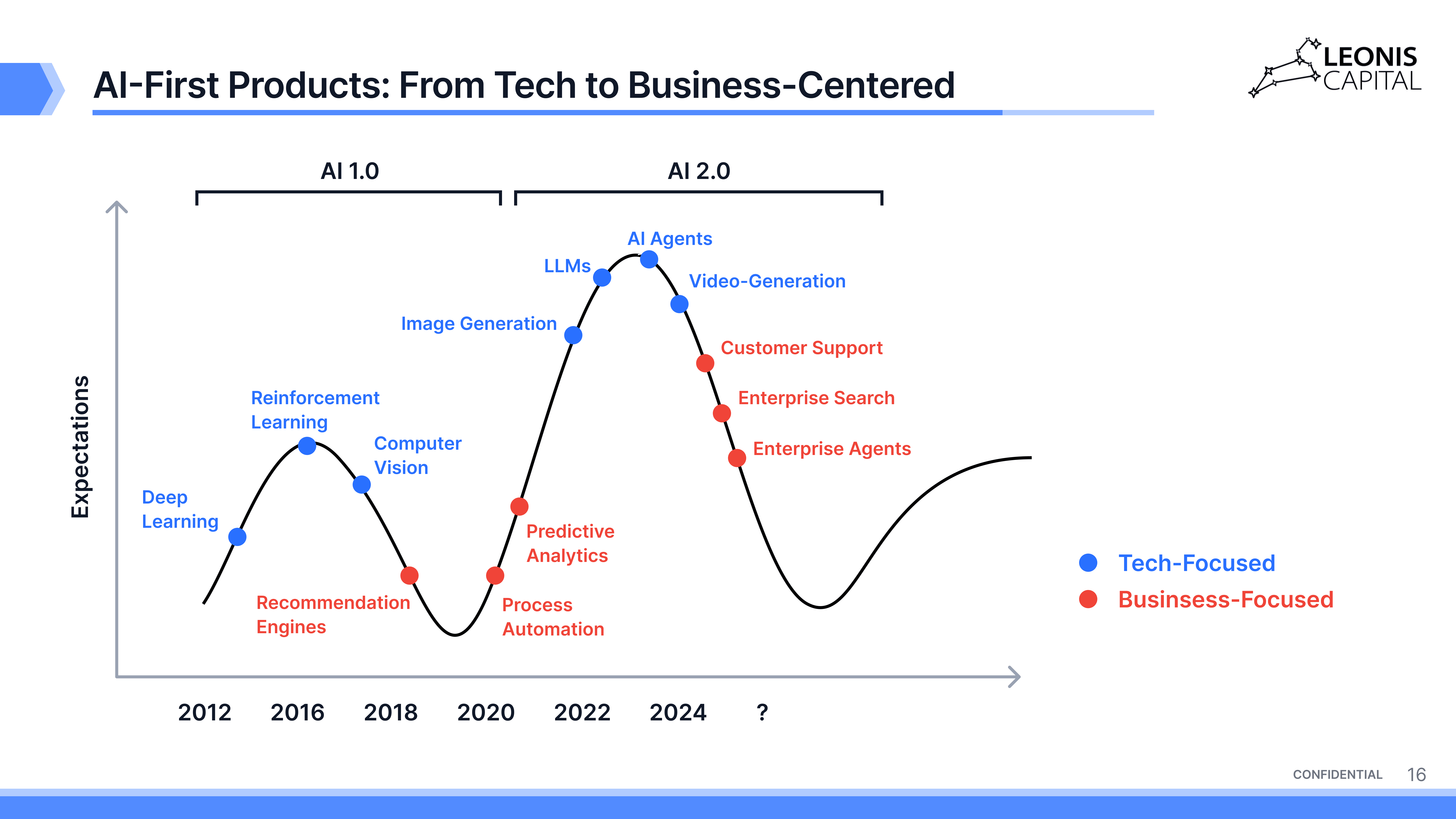

Throughout AI development, technical and market considerations fluctuate within a hype cycle. Early in the cycle, founders and investors focus on technological advancements and new business models. As the technology matures, traditional business metrics like ARR and ACV gain prominence.

In AI 2.0, we are currently transitioning from a tech-focused phase to a business-focused phase. The end game for the “sexy new generative AI” is “good old enterprise SaaS.”

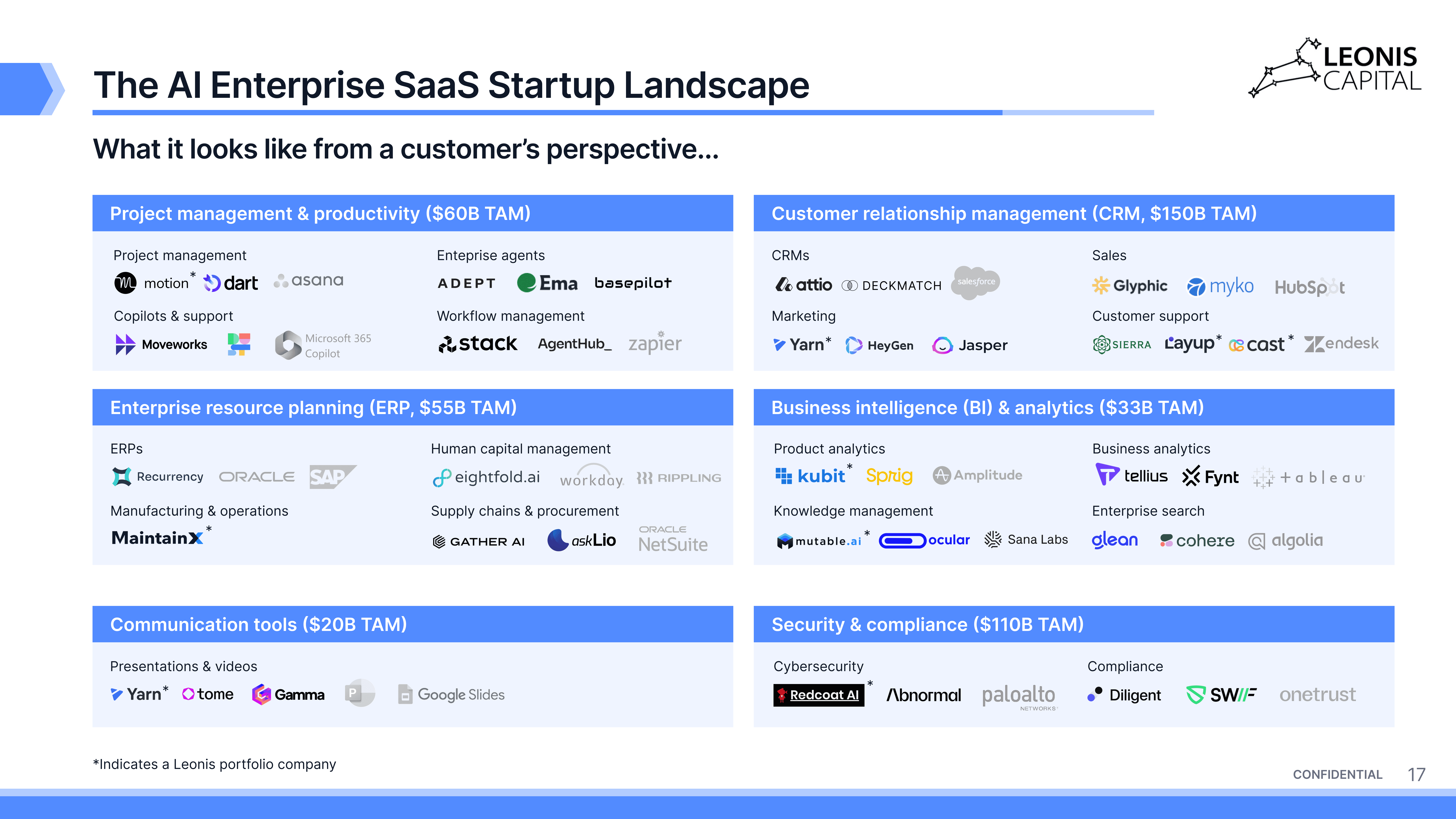

This shift has changed our view of the AI startup landscape. Our 2022 market maps categorized AI startups by modality—text, audio, image, or video. This year, we present the enterprise customer's perspective, focusing on software categories that enterprise buyers are purchasing and their options.

We could spend entire sessions or blog posts discussing individual sectors in enterprise SaaS, but the main takeaway is simple: AI companies have large markets to conquer. We believe these companies can move faster than their traditional SaaS counterparts due to their tech stack and talent advantages. We are already seeing this type of market value transition from the AI 1.5 companies we track—the speed will accelerate as AI 2.0 companies become more stable and mature.

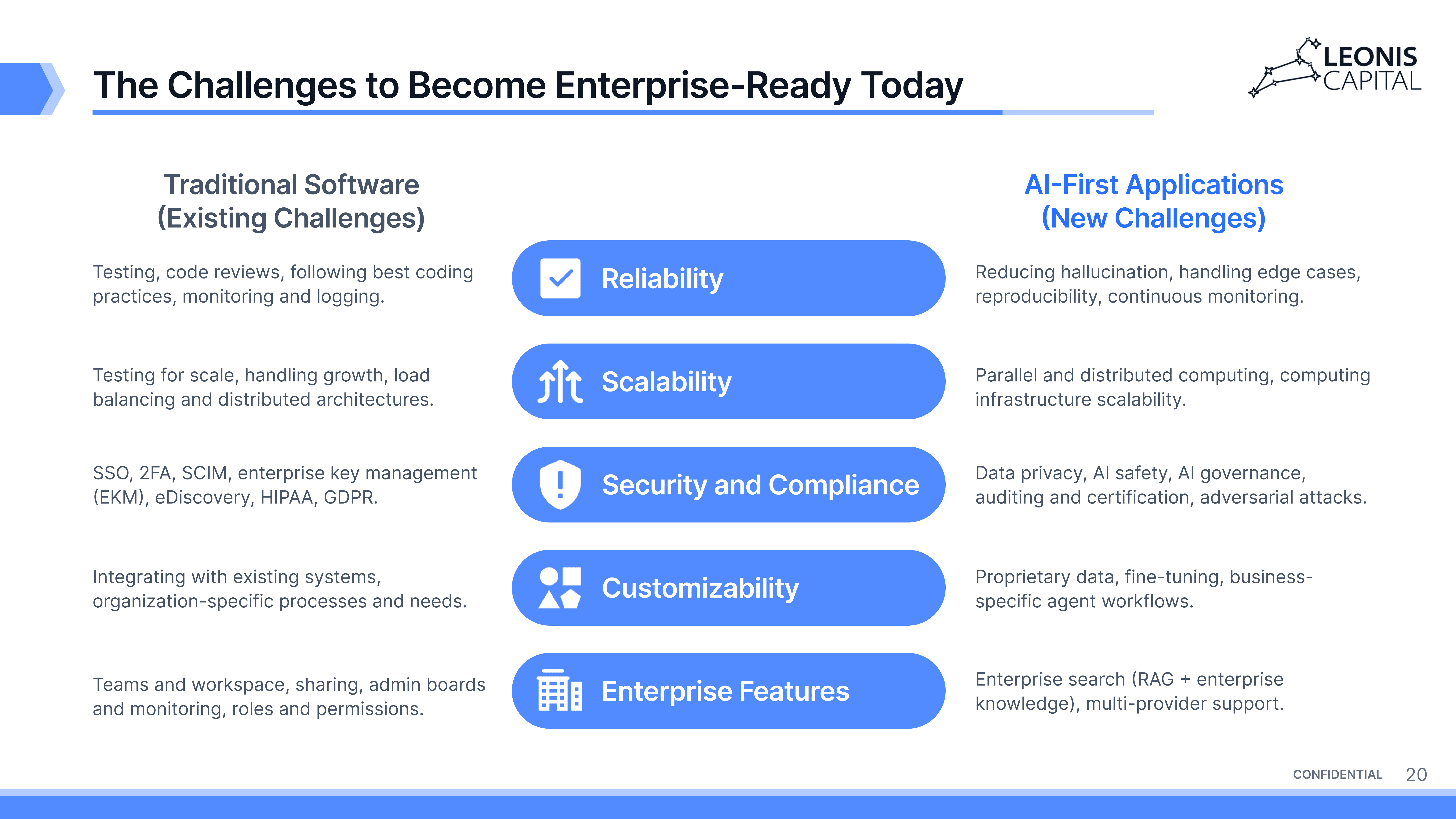

However, these AI-first companies will also face challenges in their building enterprise-ready products. We summarize these challenges as follows, based on our observations of our portfolio companies:

Across all five categories of challenges — reliability, scalability, security and compliance, customizability, and building enterprise features, AI-first companies will have to overcome traditional challenges while tackling the new challenges brought about by AI. Luckily, over time, these challenges are made easier as more developer tools are introduced to solve these specific issues.[1]

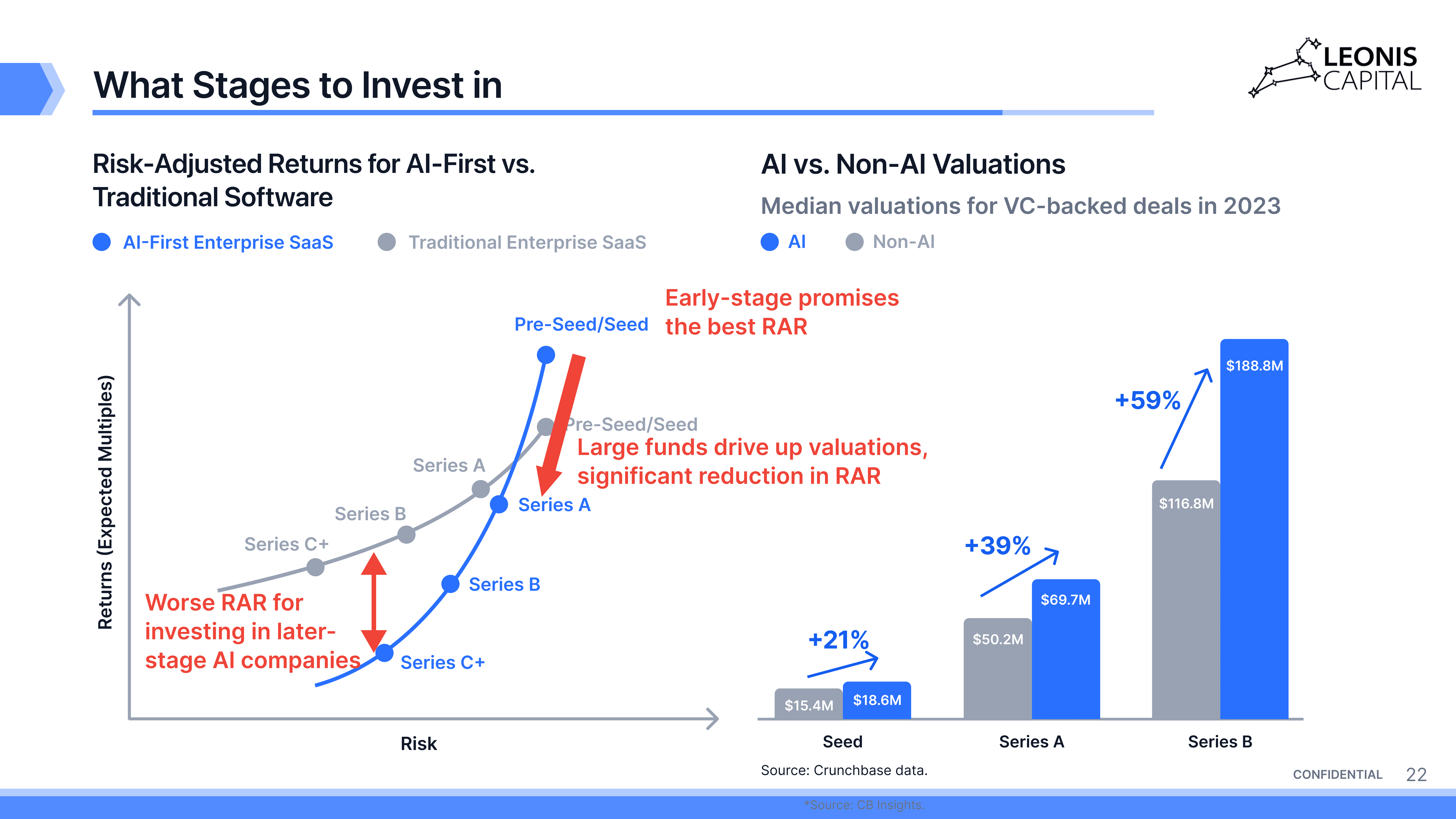

The final part of our thesis addresses the question of what stages to invest in.

For AI, we believe that seed and pre-seed stage companies offer not only the highest potential returns but also the highest risk-adjusted returns. This is not solely because large funds entering the market drive up Series A and Series B valuations. More importantly, as mentioned earlier, AI 1.5 and 2.0 companies tend to have a stronger ROI and a more intuitive value proposition. Therefore, when they hit product-market fit (PMF) around Series A, the inflection points become even more apparent than in traditional SaaS companies. Consequently, most of these companies attract multiple term sheets from downstream VCs, which often commoditizes larger funds’ investor capital and further drives up valuations as the companies scale into the growth stage.

Next Session Preview: AI-First Vertical SaaS

In our next webinar session, we'll discuss AI-first vertical SaaS companies. While enterprise and vertical SaaS share similarities, they also have distinct market dynamics and challenges. We'll focus on three verticals—finance, healthcare, and legal tech—and explore how AI can transform these sectors. Until next time!

Footnotes

[1] This also presents an opportunity for developer tool companies, as more companies are looking to adopt AI.

Be the first to know about our industry trends and our research insights.

Our latest insight decks on technological and market trends.